Our Market Operations Weekly Report contains the latest information about the electricity market, including security of supply, wholesale price trends and system capacity.

It is published every Tuesday. Click here to receive the report via email every week.

If you have any comments or questions please contact the Market Operations Team at [email protected].

Latest Report / More Information

|

Image

|

|

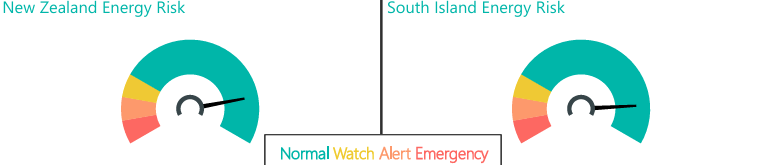

Current Storage Positions

Overview

National hydro storage remains above average at 134% of the historic mean for this time of year. Residuals have been below average due to the increased demand and calmer low wind periods during the peaks.

In this week's insight we detail the Low Residual Customer Advice Notice (CAN) sent before Wednesday's morning peak and some of the risks that we consider before issuing these notices.

Security of Supply and Capacity

Energy

National hydro storage has remained at 134% of historic mean at the end of last week. South Island storage has increased from 135% to 137% and North Island storage decreased from 120% to 111%. Storage levels remain well above average across both islands, supported by continued above-average inflows into the South Island catchments.

Capacity

Residuals have been less than average with the increasing demand and lower thermal unit commitment linked with high hydro storage. The lowest residual of 324 MW occurred during the evening of Monday 20 July. Wednesday morning

reached 442 MW after the wind picked up and industry responded to our CAN.

The N-1-G margins in the NZGB forecast show tighter spots continuing as we are now in winter; we recommend the industry watch these closely. Within seven days we monitor these more closely through the market schedules. The latest NZGB report is available on the NZGB website.

Electricity Market Commentary

Weekly Demand

Total demand increased from 825 GWh last week to 875 GWh this week. The highest demand peak of 6,620 MW occurred at 6:00 pm on Sunday 26 July during. Demand doesn't usually peak this high on a weekend and signifies the beginning of the national cold snap for the week to come.

Weekly Prices

The average wholesale electricity spot price at Ōtāhuhu last week increased from $20/MWh the week prior to $64/MWh. Wholesale prices peaked at $202/MWh at Ōtāhuhu at 4:30 pm on Wednesday 22 July.

There has been significant price separation between the North and South Island due to high HVDC transfer going northwards. The reserve price separation was highest at Sunday 26 July 1:00 pm.

Generation Mix

Wind generation decreased from 13% of the generation mix to 7%. Hydro generation contributed 65%, above its yearly average of 60%. Thermal generation increased from 1% of the mix last week to 3%. Geothermal generation decreased slightly to 23% last week.

HVDC

HVDC flows last week were entirely northward. Overall, 247 GWh was transferred north. There were several periods of inter-island energy and reserve price separation due to the high HVDC northward transfer and the HVDC link setting the North Island risk. The highest northward transfer was 1120 MW on Sunday 26 July 11:30 am.