The Energy Security Outlook (ESO) is a monthly report that helps track how secure New Zealand’s electricity supply might be over the next two years. It uses two key tools, the Electricity Risk Curves (ERCs) and Simulated Storage Trajectories (SSTs), to show how likely it is that we’ll have enough electricity, especially during dry periods when hydro lakes are low.

For more information on how it works and why it matters, we have published an 'ESO 101' document that covers how ERCs and SSTs help forecast electricity risks, what triggers action when supply looks tight, and how extra hydro storage can be used if needed.

July 2026 Energy Security Outlook

The Electricity Risk Curves are evaluated through two lenses: the Fuel Capability Case (Base Case), which uses the original methodology based on total physical capability to source thermal fuels and utilise it for generation, and the Contracted Fuel Case, which strictly limits thermal energy to firm commercial contracts secured by generators. This approach highlights the gap between physical capability and actual commercial certainty, signalling to industry where additional fuel contracts can yet be secured to reduce security of supply energy risks.

On 3 July Meridian received consent for their fast-track application to access what has been considered contingent storage in lake Pūkaki without an Alert or Emergency status being declared. This consent will expire on 31 December 2028. Once this consent is effective, it will impact the ESO by lowering the Alert and Emergency risk curve floors and by lowering the SSTs on average to reflect the lower expected operating levels for lake Pūkaki with unrestricted access below 518m RL (down to 513m RL). However, the consent has conditions which must be met before it can be exercised and it will take Meridian some time to meet these conditions. As such, the effect of the consent is not modelled in this ESO update.

- Base Case

The Fuel Capability Case (Base Case) assumes the market supplements the existing coal stockpile at its maximum import capability to maintain increased thermal generation during any extended periods of low hydro inflows.

Overall, there have been reductions to the risk curves for 2027 due to a combination of:

- Small increases in current gas and coal storage levels.

- An increase in expected starting gas storage levels in 2027, following the temporary shutdown of Huntly Unit 5 to make gas available to other users.

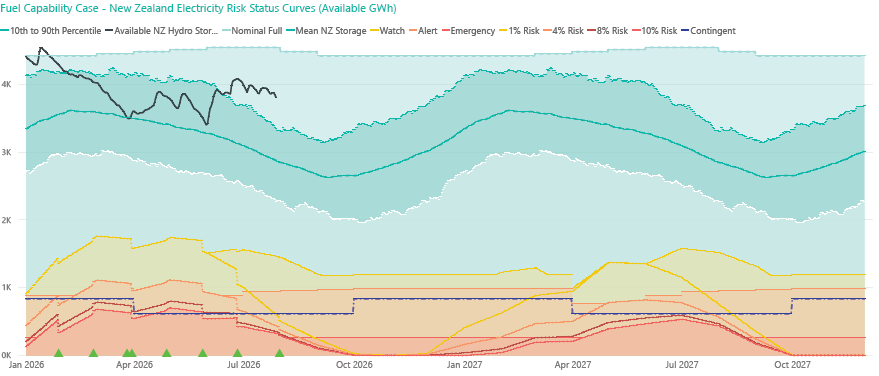

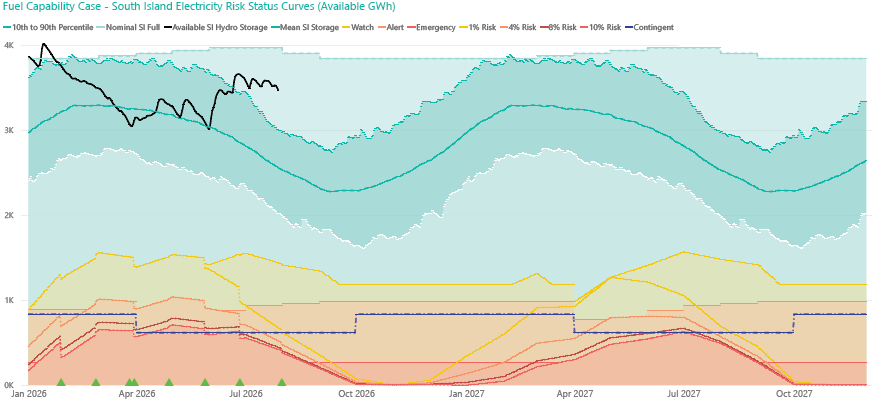

No Simulated Storage Trajectories (SSTs) cross any curve in 2026 or 2027. This indicates a low risk of hydro storage depletion under expected market response.

The national controlled hydro storage position is currently 132% of the historic mean with South Island storage at 136% (at 29 July), providing a strong energy storage position for the current winter. Earth Sciences NZ (formerly NIWA) has confirmed that El Niño conditions have been reached. The July-September Climate Outlook is for "normal or below" or "below" rainfall for most of the country except for the western South Island, where rainfall is most likely to be above normal. Earth Sciences NZ predicts about an 80% chance for El Niño to reach or exceed strong intensity, and expects the El Niño influence to become more apparent later in the season. These conditions could improve inflows into major SI catchments in the western South Island.

Industry’s ongoing focus on hydro storage management and ensuring sufficient backup thermal fuels and capacity through winter continues to mitigate the potential for sustained high prices.

The graphs below compare New Zealand and South Island base case controlled storage to the relevant Electricity Risk Status Curves.

Image Image

Image

- Contracted Fuel Case

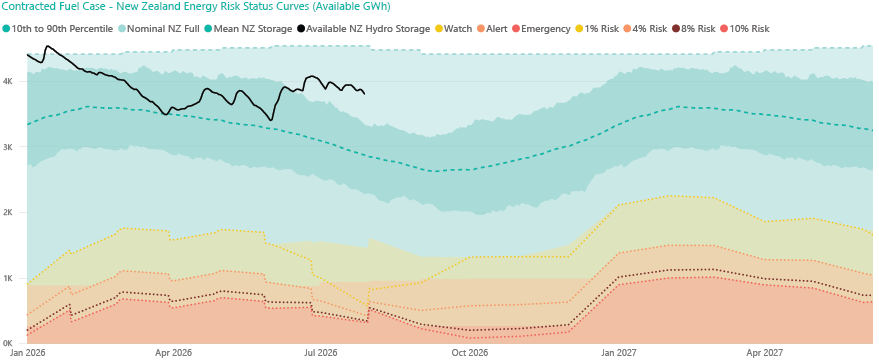

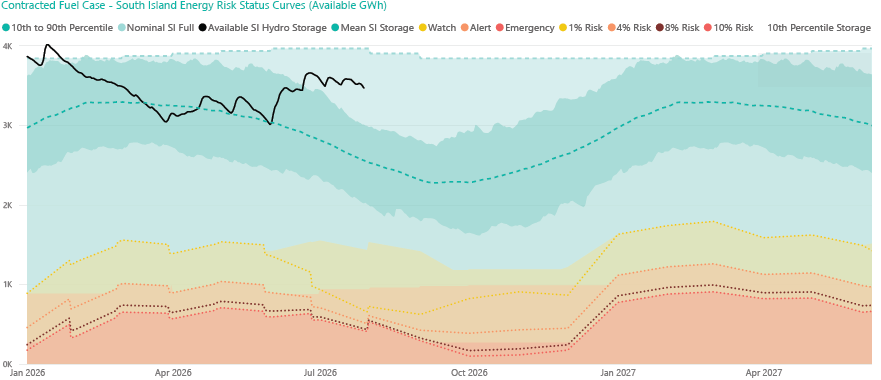

The Contracted Fuel Case assumes that only thermal fuel supplies currently secured through contractual arrangements are available for generation. Current thermal fuel

contracts are sufficient to fuel most of the power system's thermal generation capability in 2026, reflecting a strong near-term contracted fuel position. As a result, the

Contracted Fuel ERCs for 2026 are similar to the Fuel Capability ERCs.Should extended dry conditions emerge in 2026, additional thermal fuel contracts can help reduce the risk curves and raise the SSTs. The risk curves can reduce by up to 220

GWh or 39 Rankine days.The gap between the Contracted Fuel Case and Fuel Capability Case risk curves becomes more pronounced in 2027 (diverging by up to ~1000 GWh or 180 Rankine days). This results in some SSTs crossing the Watch curve (5 for the New Zealand Watch curve and 2 for the South Island), reflecting the market's tendency to contract fuel closer to need.

By restricting available energy strictly to currently secured contracts, this Contracted Fuel Case intentionally highlights the physical capacity that remains uncontracted, and the

ability for additional contracting to reduce risks. This reinforces that contracted positions require continuous updating to provide ongoing security of supply cover.The graphs below compare New Zealand and South Island Contract Fuel case controlled storage to the relevant Electricity Risk Status Curves.

Image Image

Image

Related Files

Energy Security Outlook Data Files

Assumptions and Update Logs

- Scenarios

- Historic Logs/ Reports