Our Market Operations Weekly Report contains the latest information about the electricity market, including security of supply, wholesale price trends and system capacity.

It is published every Tuesday. Click here to receive the report via email every week.

If you have any comments or questions please contact the Market Operations Team at [email protected].

Latest Report / More Information

|

Image

|

|

Current Storage Positions

Overview

National hydro storage remains above average at 134% of the historic mean for this time of year. Residuals remained healthy despite low thermal commitment with demand well below the peaks seen in recent years. Wholesale prices were also at their lowest July levels in four years.

In this week's insight we look at what today's intermittent generation would have contributed to Aotearoa's highest demand peaks over the past five years.

Security of Supply and Capacity

Energy

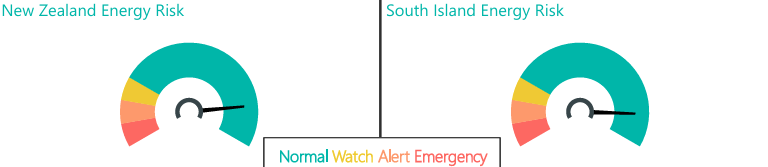

National hydro storage has increased to 134% of historic mean at the end of last week from 130% the week prior. South Island storage has increased from 128% to 135% and North Island storage decreased from 123% to 120%. Storage levels remain well above average across both islands, supported by above-average inflows into South Island hydro catchments during the week.

Capacity

Residuals were healthy during morning and evening peaks last week. The lowest residual of 880 MW occurred during the morning of Monday 13th July.

The N-1-G margins in the NZGB forecast show tighter spots appearing as we are now in winter; we recommend the industry watch these closely. Within seven days we monitor these more closely through the market schedules. The latest NZGB report is available on the NZGB website.

Electricity Market Commentary

Weekly Demand

Total demand decreased to 825 GWh last week from 864 GWh the week prior. The highest demand peak of 6,535 MW occurred at 8:30 am on Monday 13th July. This is well below record peaks in recent years of just over 7100 MW.

Weekly Prices

The average wholesale electricity spot price at Ōtāhuhu last week decreased to $20/MWh from $79/MWh the week prior. This is the lowest average price in Julyover the last four years. Wholesale prices peaked at $101/MWh at Ōtāhuhu at 8:30 am on Monday 13th July coinciding with lowest residual of the week.

Generation Mix

Wind generation increased to 13% of the generation mix from 7% the week prior. Hydro generation contributed 59%, slightly below its yearly average of 60%. Thermal generation decreased to 1% of the mix last week inline with abundant renewable generation. Geothermal generation slightly increased to 25% last week, sitting just above its annual average of 23%.

HVDC

HVDC flows last week were predominantly northward with one brief period of southward flow during Saturday night. Overall, 195 GWh was transferred north, while 2 GWh was transferred south during the week. There was a period of inter island energy and reserve price separation on Thursday 16 July with very high HVDC northward transfer (at times over 1000 MW) and the HVDC link setting the North Island risk.

Consultations and Engagement

System Operator Strategy

Our Phase 2 Consultation for the development of a new System Operator Strategy is open. Responses are due by Friday 24 July 2026. The draft Strategy sets out our proposed direction for how the System Operator service will need to evolve over the next ten years to support a secure, reliable and efficient power system.